GLP-1 Check In

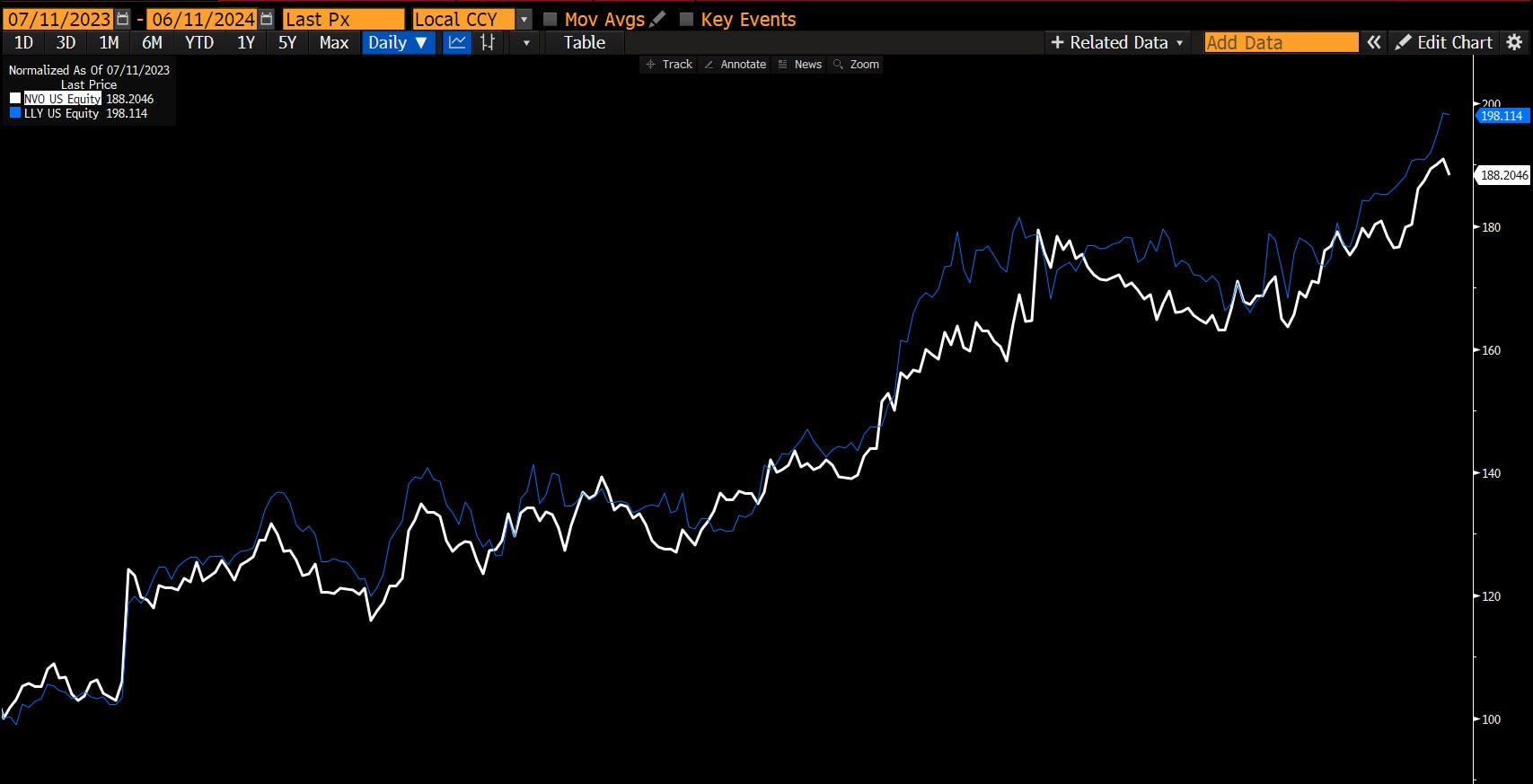

LLY +100%, Highlights from Annual Review

Eli Lily (LLY US) is now just about a double since we first wrote our GLP-1 thematic primer on July 11th 2023:

I have removed the paywall for free subscribers to go back and check it out in celebration of this milestone (simply a stepping stone on the way to LLY having a trillion dollar market cap by the end of the year).

When I went to go change the paywall, I found myself rereading my original takes on the theme and doing some reflection.

It’s easy to find out where a bad trade went wrong, but it’s arguably more important in your process to find out how you could have made a good trade go better as well.

I figured it would be a good exercise to go back and assess my original thought process and see which parts proved accurate and which didn’t.

Upgrading from Overweight: The Effects of GLP-1 Drugs on the Investment Landscape

Upgrading from Overweight: The Effects of GLP-1 Drugs on the Investment Landscape The Questions: GLP-1 Drugs and Obesity If you haven’t, please read my article on Thematic Investing & Megatrends here fi…

There were three things that, going into this process, I was concerned aged poorly.

The first was WeightWatchers: I personally did quite well on WW because I sold about half my position with a +95% gain, then exited the rest when it was at my original cost basis. I had gotten in with my eyes open that this was a high risk high reward play, but I was concerned that I hadn’t conveyed that clearly enough in the article.

I was pleasantly surprised when my re-read reminded me that I was very clear about exactly why WW could work:

All good on the first concern!

Second, of course, was Health Insurers. I was too long term & contrarian on my views on HMOs like UNH & HUM. It was the wrong call, no two ways around it.

The good thing is that I was not insistent on keeping them in our basket and hit the eject button when this became clear. We ended up removing these from our long side in our portfolio review at the end of 2023 and were spared the worst of their slaughter, it is important to assess why this was wrong (and whether it will still continue to be wrong).

While I was bearish on PEOs and companies w exposure to employee benefit plans like Insperity (NSP US), I figured one could go long HMOs for the long term benefits (whoever took the biggest hit in the short term on paying for GLP-1s would ultimately reap the biggest reward in the long term on a healthier customer base). While this trade wouldn’t have lost you money, it definitely did not make you a ton and the fact of the matter is that opportunity cost is SO high when you’re presenting an idea in a primer that is focused on “check out this massive money printer” essentially.

Overall, it seems that until the pricing edge is lost by the NVO/LLY duopoly its best to steer very clear of insurers but down the road once they are cheaper I would be quite interested in assessing the ones who have been hit hardest in the market for the highest volumes of early GLP-1 coverage as I believe they could make outsized returns on a comeback given the longer term benefits they will begin realizing on their bottom line sooner than peers. For now, we still stay away.

Third was my Emphasis on Archetypal Winners: Even though I know how these trades did (quite well), they also necessitated a level of “trading in and out” due to the volatile environment in rates that most medtech companies are extremely sensitive to. My primary concern was this: “did I make it painfully obvious that LLY and NVO were the clear winners and, if you were only going to execute one single trade after reading this that trade should have been long one or both?”. I always try my best to present themes in the way I like to play them (broader basket encompassing most likely winners against short most likely losers, best attempts to neutralize factors and isolate returns associated with the theme) and then an outline within that of the archetypal winner.

You should know these by heart if you’ve been a subscriber for longer than a couple months.

If not, they are: LLY/NVO in GLP-1 thematic, NVDA/Hyperscalers in AI thematic, ETN in Fiscal Primacy thematic, ECL in H2O, people who enjoy complaining in Election thematic (kidding…well, I wouldn’t be if we could securitize complaining).

This involves a kind of implicit wink. You can read it as me saying something like the following:

I know you’re going to ask me so, yes, you can forgo the basket construction I am so fond of and just make this single name your whole position. With some caveats:

You will have a better chance at realizing insane returns but also a high likelihood of realizing a degree of volatility that ultimately will make it more likely that you capitulate your position at the wrong point of this multi-year long trend,

This will require you to focus more on the single name idiosyncrasies rather than the broader properties of the thematic trend and you will need to delve deeper into “security analysis” rather than “thematic trend analysis”. Your exposure to the ups and downs, ins and outs and weird little ticks associated with a single public company will be markedly higher and you will need to ensure you are well-versed in these, because of that realized volatility I spoke about. It’ll be very unlikely our thematic basket is ever down 10% in a single day, but a single name can always drop like that (even on BS rumors).

Your own exposure & equity curve will give you less of a comprehensive read into how the thematic trend is performing and you may lose out in the long term from benefits that are secondary and tertiary to the thematic rather than just primary. If the primary winner is disrupted and bested by another that continues the trend of the theme’s tailwind but abruptly ends the trend of the archetypal winner seeing accelerating top & bottom lines…well, that’s the bet you’ve taken.

With those caveats being said, in a year that’s been so amazing for thematic equity it’s easy sometimes to wonder why I didn’t just YOLO long LLY. (There are worse problems to have than being up 60% on a position and wondering why you didn’t make the choice that would have had you +100%). Regardless, it was important I assessed whether I had the clarity of thought & directness of language required to convey that this duopoly was the clearest expression of GLP-1s winning.

I do believe that I conveyed that accurately in the article;

Some other areas that aged like milk in comparison to our LLY+NVO call aging like DRC were primarily in the more speculative areas.

We’ve established being contrarian and long term ultimately harmed us when it came to including health insurers in our basket. We also had a bit too much in the way of speculation when we had the idea that MTCH & BMBL would be helped by GLP-1 assisted weight loss - that was a failure for sure.

While our speculations on secondary effects for the short side were relatively spot on, as we will discuss later, it seems out of 3 of the more speculative and slightly contrarian secondary beneficiaries (I.e. not manufacturers/sellers) we had about two out of four really worked: CURV and ESTA.

When I originally wrote the article I highlighted the idea that the limited available coverage of this theme discussing second order impacts (it really was quite limited at the time of writing - nothing like two months later when it had progressed to “what if people are less fat so airlines use less gas???”) had mentioned the potential for negative impact on the plus size clothing outlets.

I theorized it was actually the opposite:

“If you lose 20% of your body weight in a year, you’re going to be doing a lot of clothes shopping unless you want to look like someone threw a sheet on top of you and you decided that was dressing. I think that, especially in the beginning (right now) as these drugs are gaining notoriety and seeing increased usage, it’s tough to say but in the short-term, those plus-size clothing stores may actually see an increase in demand. As people who are losing weight need to purchase new clothes that fit their changing bodies, this could result in a temporary surge in revenue for clothing retailers, including plus-size specialists who often cater to a broad range of sizes. Additionally, as noted earlier, there is a risk that there is a rebound in weight.”

Looking at the failed speculative plays I can pat myself on the back for what actually matters in this game: risk management. I look at health insurers or our plus size clothing long that did not work (DXLG) or our long on INMD or MTCH/BMBL. All of them we cut without sitting through more than a -30% drawdown. The longest we sat through a drawdown was on STVN which I probably got too attached to the story on.

ESTA was a more speculative play aimed at rectifying the disaster that was INMD. While INMD’s product actually sucked and wouldn’t even actually benefit at all from increased abdominoplasty rates, ESTA’s product is quite good and we managed to get in before the market was fully aware.

So the takeaway from the GLP-1 longs is that we should have really focused a lot more on the duopoly, because we knew from the beginning that would be the best way to play. There’s a reason I ended up overweighting them so significantly - but it’s a solid thing to keep in mind and learn from. If I was going to describe how each side of this basket performed in terms of quality of ideas, I’d say the long side’s ideas were best from primary effects of GLP-1s and the short sides ideas worked best when focused on secondary effects.

We can see that by looking at the returns if we had equally weighted every single short we ever put on in the basket and then comparing that to the performance of the benchmark:

Our shorts down more than 31% while the S&P500 is up more than 20%. That’s a successful romp on the thematic short side for sure.

This is because the negative secondary effects were much more immediate, I believe.

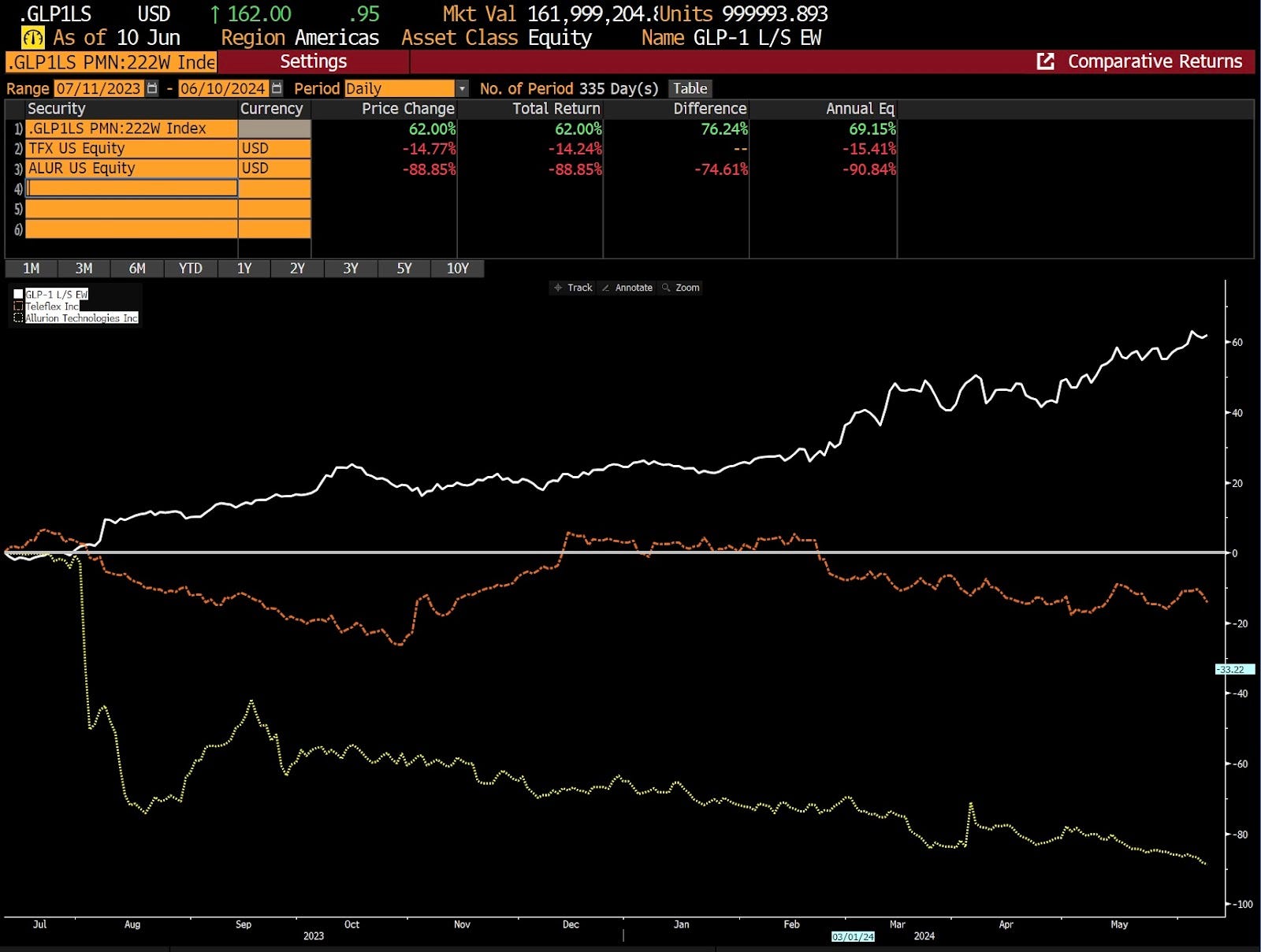

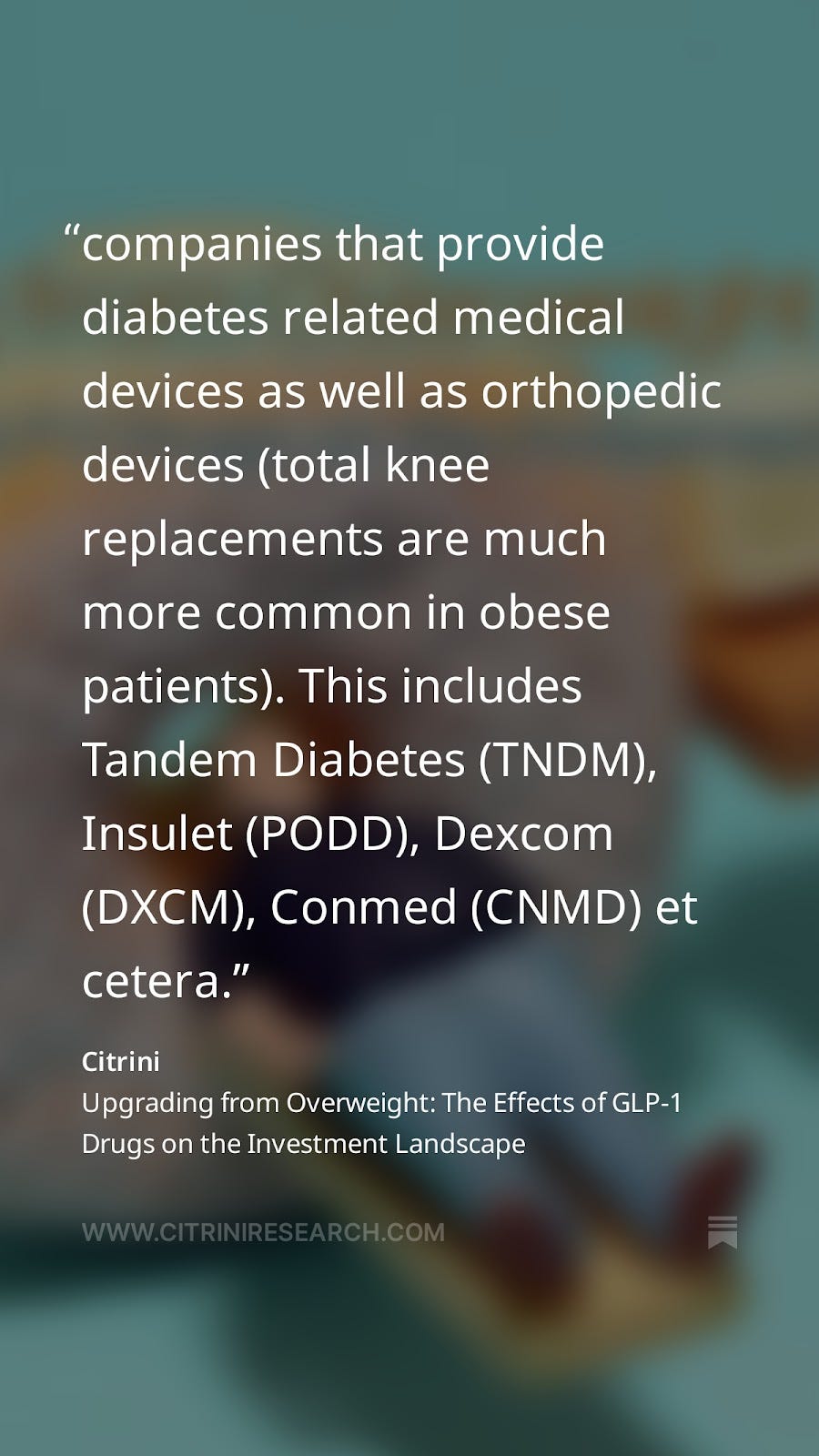

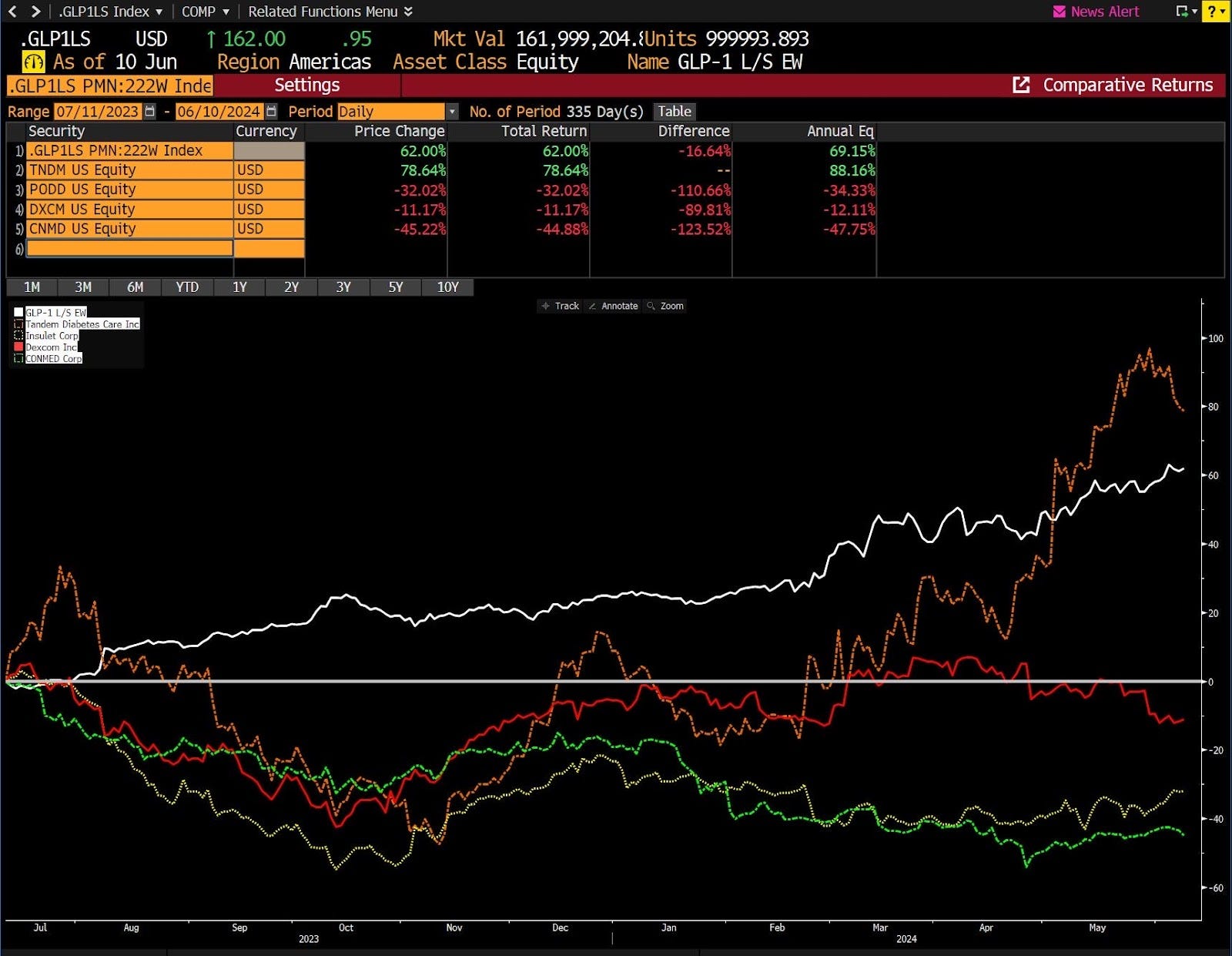

BARIATRIC AND DIABESITY

I had a lot of fun making fun of the TITAN STAPLER but the thing is that you can’t attribute to GLP-1s what you can attribute to interest rates. The reason why we hit the eject button on most of these shorts at the end of October was because a rate rally could have (and would have) squeezed us. I think you’ll continue to get a secular decline here and a couple are good permanent shorts but mostly you have to trade around it while rates still are volatile. You can also see that our cover on TNDM was quite well timed, I actually may consider putting that short back on now.

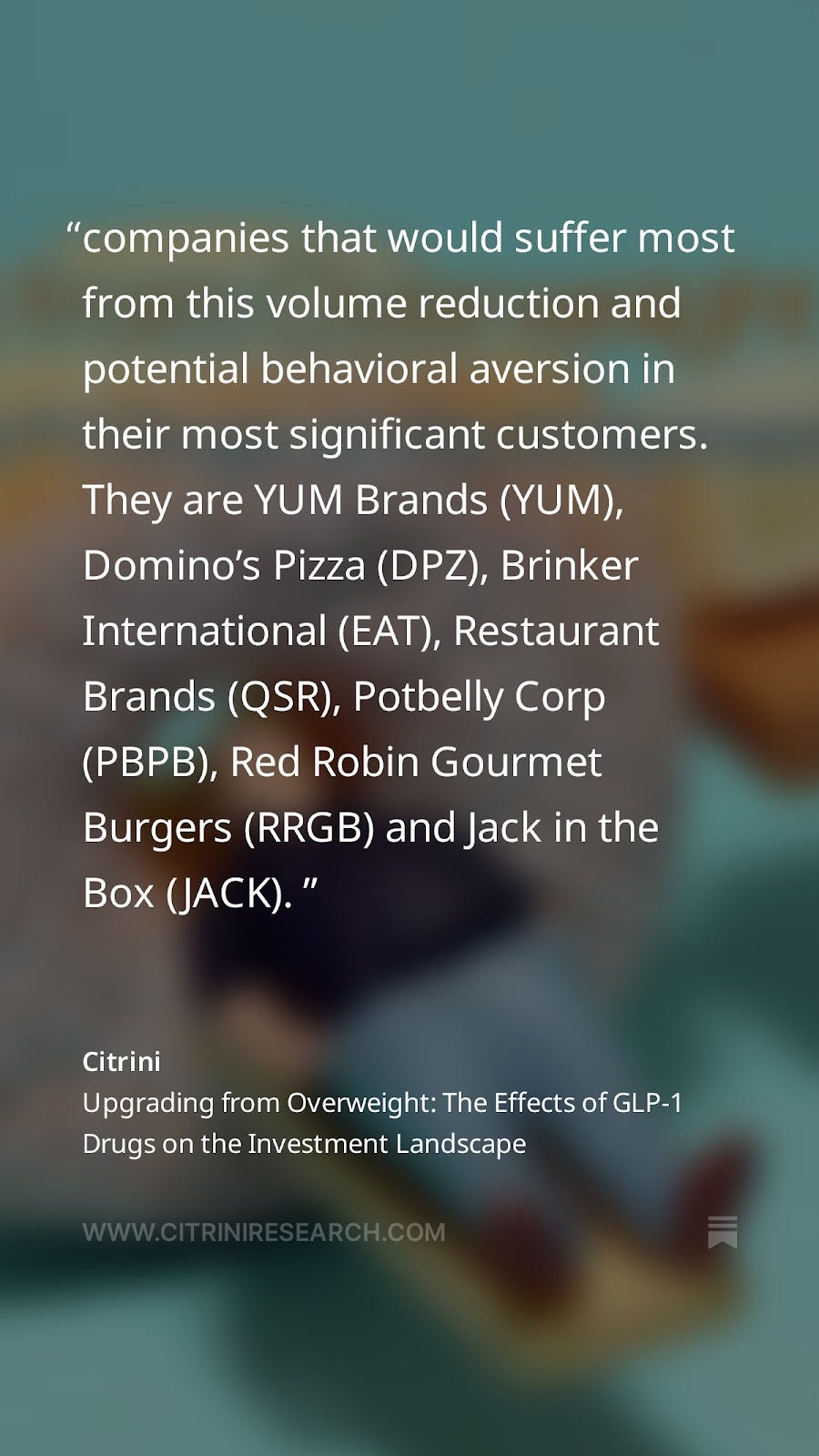

CALORICALLY DENSE SHORTS

Let’s look at how our healthy fast casual food longs have done versus our main shorts on greasy calorically dense fast food and fast casual:

.FSTFOOD is the fast food shorts we discussed in the July 2023 primer.

HEALTH AND WELLNESS

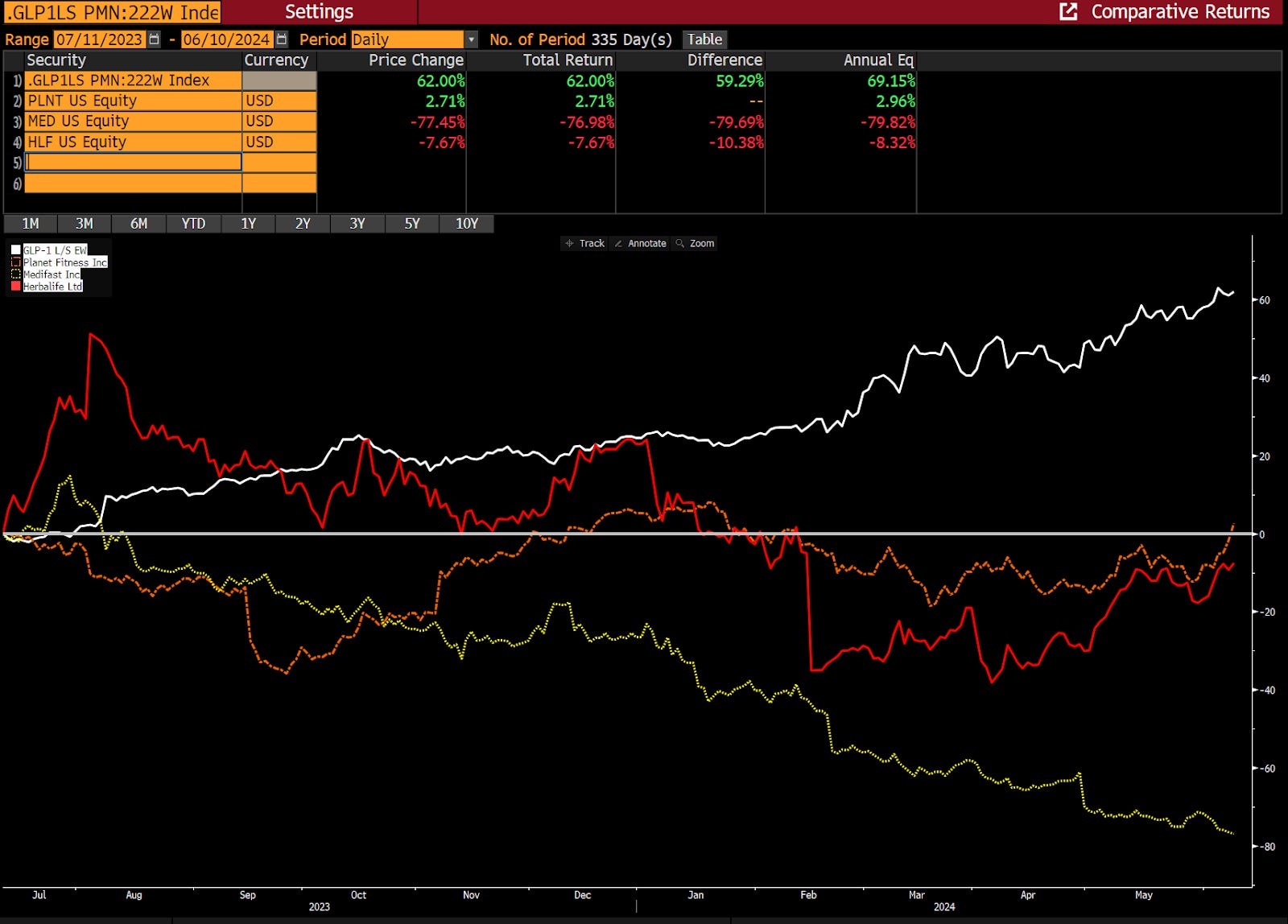

This contained our most successful short: MediFast (MED US).

SLEEP APNEA

These also have been a bit volatile but excellent shorts.

Below the paywall, I’ve highlighted the main points of our 1 year annual review for our key themes as they relate to GLP-1s.

If you enjoyed this preview, please consider becoming a paid subscriber!