For our annual review, I covered every theme we’ve written about in the past year since CitriniResearch began. This included AI Winners & Losers, GLP-1s, Fiscal Spending, Water and the 2024 Election to name a few. I’ve included a free excerpt of it below. But first…

To celebrate the 1 year anniversary, I’m running a 10% discount on annual subscriptions to CitriniResearch (which will lock in forever even when the price goes up in the future). This promotion will last for until Friday.

A year ago, when CitriniResearch began, I started off at $400/year and increased the price by 10% every month. Whenever a free subscriber upgrades to paid, their price is locked in for life. That means even when I’m charging thousands a year, you’ll be locked in with this discount.

I hope you’ll consider subscribing!

Regardless of if you do, I’m including a free excerpt from our last piece - my thoughts on China and our Chinese Equity allocation in the Citrindex.

Enjoy, and thanks for subscribing!

Thematic Review: Thoughts on China

Market sentiment has seen an uptick following several positive initiatives by policymakers. Recent measures, including a relending program aimed at alleviating housing market inventory pressures, have bolstered sentiment.

I have been buying this recent dip as I believe it will be short lived.

Looking ahead, I expect that there will continue to be gradual increased fiscal and monetary support and place the likelihood of a “firehose” stimulus plan at about 20% (although this would require some volatility first to show that existing measures are not working).

Our decision to take off the CNH hedge was a good one but I think the thesis is still valid vis a vis the asymmetry in equities vs. the effect stimulus will have on the currency, so I will continually be monitoring to put it back on.

Three critical policy events to watch include:

1) The Third Plenum in early to mid-July;

2) the quarterly Politburo meeting towards the end of July; and

3) the Central Economic Work Conference in December 2024.

In the China basket, we move to protect our holdings from any trade war headlines that could negatively impact export-focused businesses and continue to expect measures to more heavily favor the domestic economy. This includes names in semiconductors, consumer discretionary with high domestic revenue and some industrials.

While the entire Chinese economy arguably hinges on the property market, we have been cautious about adding too much direct exposure - the only property developer in our basket was Sunac. Now, with the government appearing more willing to take steps necessary to attract foreign direct investment and support both the market and the economy, I believe we can take a shot at adding BEKE as well. Their recent earnings report showed revenue meeting expectations and EPS above consensus. Demand may see a boost in the second half, and the company’s R&F and home rental businesses could see renewed growth.

KEY TAKEAWAYS:

CHINA LOCALIZATION: EFFORTS FROM CHINESE STIMULUS FOCUS ON BOLSTERING DOMESTIC ECONOMY RATHER THAN EXPORTS,

TAKE STEPS TO GUARD OUR CHINESE EQUITY BASKET FROM A TRADE WAR

GAIN UPSIDE FROM CHINESE EFFORTS SEMICONDUCTOR INDUSTRY DECOUPLING – LIKELY TO SEE INCREASED GOV’T SUPPORT

Imagine being a hyperscaler right now and reckoning with the fact that NVDA essentially has you by the balls.

At the mercy of their pricing, you would consider spending some money on developing your own silicon (in the form of ASICs). Now, you’d also have to consider the fact that there may be higher ROI in simply biting the bullet, paying up to NVDA for now and prioritizing using their products to build out your own AI capabilities. Would you spend more on custom silicon or on buying NVDA chips to improve your own AI? Well, considering you run the risk of falling behind your competitors and being in a position where your own product doesn’t even advance enough to justify custom silicon if you don’t do the latter, we probably know your choice. Of course, all the hyperscalers are interested in custom silicon that will free them from the blackwellian yoke of oppression, but they are focused right now on the potential for AI to improve their own businesses and that likely informs their priorities.

Now imagine you’re kind of a hyperscaler but the nation-state version. This concept is also known colloquially as “China”.

You can’t buy NVDA chips. I mean, you can. But not on the scale that you really need to. Sanctions aren’t 100% effective for everything, but sanctions on a product that has red hot demand like the most cutting edge NVDA GPUs are pretty damn effective.

China faces what could be perceived as a national security issue - a state of emergency where, if NVDA chips result in the US developing military technology that can outplay them in either a physical or virtual battlefield they have no real method of catching up, let alone attempting to surpass their foe.

The answer here is pretty straightforward. You’re going to have to create your own NVDA chips. That’s kind of insane, though, because NVDA chips are the result of decades of R&D with a unifying goal and are supported by deeply ingrained relationships. For the first time in a while, China’s technological answer does not seem to lie in copying innovations elsewhere. That’s worked for quite a while, but it won’t work here.

Let’s not delude ourselves - China probably has the exact specs and process information necessary to make a hopper chip. There’s no way that corporate espionage would have whiffed that badly. What they lack is the capability to create everything that makes it work so well.

China is going to have to continue spending aggressively on WFE and redouble their efforts in AI on finding a way to get on without the NVDA handicap.

Remember crypto mining? For the longest time (after the hash got too complex to solve on your PC’s CPU) if you wanted to mine crypto you’d get a motherboard, some pci-e risers, 6 NVDA GPUs (probably 1080s, this was a while ago) and stand them up in a milk crate. Behold, the instrument of great wealth (in 2017):

Eventually, however, some Chinese companies figured they could do this better. The advent of specialized ASIC miners from Chinese companies like Bitmain and Canaan Creative changed the game. These purpose-built machines were far more efficient at mining than a rig of NVDA GPUs, and soon became the standard for serious miners. This shift demonstrates the potential for China to innovate its way out of the current AI hardware predicament.

However, the challenge China faces with AI chips is orders of magnitude more complex than crypto mining ASICs. NVDA's GPUs are not just powerful number crunchers, but are supported by a vast software ecosystem, optimized libraries, and a thriving developer community. China can't just spin up a few fabs and churn out knockoff Hopper chips - they need to create an entire stack that can compete with NVDA's offering.

This is where China's strategic investments come into play. By pouring money into semiconductor manufacturing equipment, they can build the infrastructure necessary to produce cutting-edge chips at scale. And by focusing their AI research on techniques that are less reliant on NVDA-style hardware, they may find novel approaches that leapfrog the current paradigm.

Make no mistake, this will be an uphill battle. NVDA's lead is substantial, and the US sanctions are a formidable obstacle. But if there's one thing we've learned from China's rise as a technological superpower, it's that they are not to be underestimated. With the right investments and a bit of that trademark Chinese ingenuity, they may yet find a way to close the gap and assert themselves as a leader in the AI arms race.

This is the thesis I have some degree of confidence in - that China will not take its artificially intelligent death like a sheep. However, if you’ll permit me some digression, I’d like to pontificate a bit on the potential environment if - let’s say 2 years from now - China manages to create ASICs that can unseat the GB…well, we’re averaging a new Blackwell every 12 months or thereabouts, so I guess GB400. What does that look like?

If China successfully creates custom AI ASICs that can rival NVDA's offerings, they will face a strategic decision on whether to sell them globally or keep the technology exclusively for domestic use. There are compelling arguments for both approaches.

On one hand, selling these hypothetical Chinese AI chips globally could have several benefits:

It would help to recoup the massive R&D investments required to develop the chips.

It could establish China as a leader in the AI hardware market, giving them more influence over the direction of the industry.

By commoditizing AI compute, China could accelerate the global adoption of AI technology, creating new opportunities for Chinese AI software and services companies.

It would be a powerful way to strike back at the US for the NVDA chip restrictions, undermining a key American advantage in the AI race.

However, there are also reasons why China might choose to keep their AI chips exclusively for domestic use:

AI technology is increasingly seen as a critical national capability, with major implications for economic competitiveness and military power. China may view their AI chips as a strategic asset to be protected, not shared.

By keeping the chips in-house, China can ensure that its own AI ecosystem has a significant hardware advantage over foreign competitors.

The US and other countries would likely try to restrict or ban the import of Chinese AI chips, citing national security concerns. This could limit the global market opportunity.

Ultimately, the decision may come down to how China prioritizes its short-term economic interests versus its long-term strategic goals. If the primary objective is to retaliate against the US and assert global technology leadership, then a commoditization strategy ala solar panels could be effective. But if the goal is to maximize China's own AI capabilities and protect its technological sovereignty, then keeping the chips exclusive may be preferred.

There's also a hybrid approach where China could sell a limited selection of AI chips globally while reserving its most advanced designs for domestic use. This could be a way to balance economic and strategic imperatives.

Regardless of the path China chooses, one thing is clear: the development of competitive Chinese AI chips would be a game-changer for the global AI industry and the US-China technology rivalry.

In the meantime, NVDA sits pretty, reaping the rewards of their hard-earned dominance. But they would be wise not to rest on their laurels. The hyperscalers are hungry for alternatives, and China is a sleeping giant that could awaken at any moment.

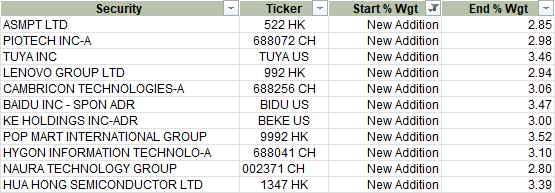

Changes to Chinese Equity Basket

In our China basket, we are also positioning increasingly in semiconductors to capture this trend of semi-localization.

These companies are expected to benefit from China's efforts to rely more on its own semiconductor production rather than importing from other countries.

NAURA: Chip-making (deposition + etching) player.

Piotech: Piotech is a rising star in the chemical vapor deposition (CVD) area, which is key in chip production.

Hygon: With a solid track record in making server CPUs, Hygon is emerging as a strong competitor to big names like Intel and AMD.

Cambricon: This company is developing top-notch AI chips and software, aiming to replace foreign suppliers like Huawei and Nvidia in the Chinese market.

Hua Hong: As a leading semiconductor foundry in China, Hua Hong is critical for manufacturing chips designed by other companies. Its role in producing a wide range of semiconductors supports China's goal of self-sufficiency in technology.

Here’s a good chart from Yole Group showing the trend in Chinese spending on WFE imports:

Additionally, I’d like to focus a bit more on China’s more ambitious initiatives that I believe will see increased funding from the government as they look to support their economy more aggressively.

This means that we’ll be buying what are effectively the Chinese answers to Nvidia (and Nvidia suppliers). Because the lead that NVDA has in GPUs is too difficult to catch up with, I believe that it’s likely that the efforts become more focused on ASICs in China. We will avoid names that are subject to sanctions like Jingjia Micro (300474 CH) and SMIC (981 HK).

I believe these additions help us to focus a bit more on China’s localized economy as a beneficiary of government initiatives in specific areas, which gives us a bit of cushion against the Tariff concerns described above. These supplement the supply-side section of our “Chinese Equity Barbell”, while we focus on names that have demonstrated solid capital allocation and growth strategies during the downturn in our more discretionary demand-side allocation.

China has bounced back a bit and, like any bear market that shows green shoots, I believe it likely that the names that held up best during the worst of the drawdown will experience a period of underperformance. These names were the “hiding places” during a bloodbath and may be used to raise funds to allocate to more beat-up names.