Microstrategy Thesis

The Short has turned into a Long…

LAST EDIT 05/30/24: The current status of my MSTR trade is I remain long 1/2 of the initial convertible bond (MSTR 0.75 2025) position originally entered on Jan 6th 2023 with a cost basis of ~52.45. The paired equity short put on to delta hedge the embedded option in March has been taken off entirely as of today. Going forward, I will remain long until these bonds are called (and may remain long the equity it converts into thereafter).

As long-time followers of my twitter account will be familiar with, the first thesis I shared on the platform was short Microstrategy in November 2021.

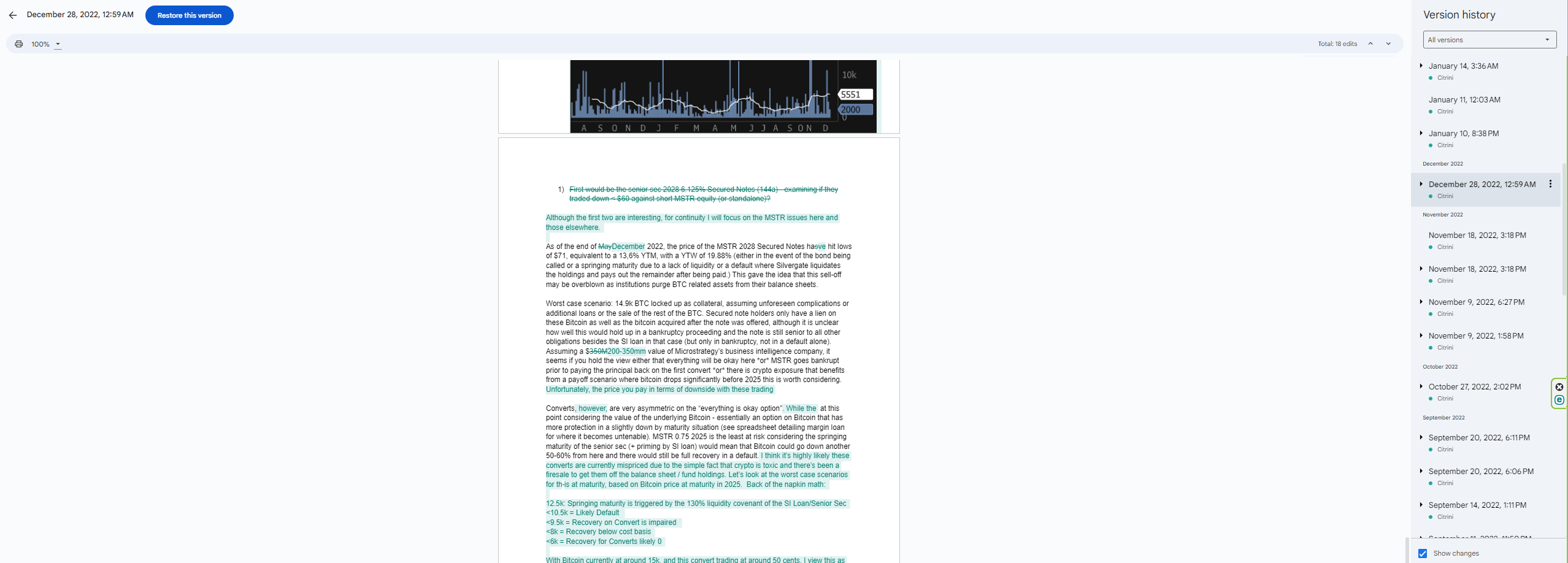

I hosted it on a google doc and have been keeping it updated since. Here, for example, you can see how I originally began contemplating going long the senior secured bonds in June 2022:

And then, as I completely exited the original short equity thesis, decided by December 2022 that I would flip and go long the converts instead, as they were extremely asymmetric. This is the state of the trade in January 2023 (long MSTR 0.75 2025 converts).

Presenting this process as it evolved was quite valuable for my own research, as the thesis morphed from:

short MSTR equity, to

short MSTR equity + long MSTR convertible bonds to

completely covering the short and being long MSTR converts as well as a couple other asymmetric bets that bitcoin wouldn’t go to zero (namely, ARBKL & ELSALV).

Now that I am publishing more long form stuff on Substack instead of just Twitter threads, I am going to take it down off google docs and put it here as a PDF:

It is, in my opinion, a good example of the pathway from idea generation to simplification with significant aspects of market sentiment awareness and position risk management. Most importantly, this was a trade where I did not make a mistake that I had made plenty of times before in short-selling: letting being short blind you to opportunities on the long side. You should always be on the lookout for opportunities on both sides in a company you’re very familiar with, especially if they’re elsewhere in the cap stack and especially if they’re as asymmetric as the converts were (arguably moreso than the equity short at $800). Shorts rarely go to zero, when you cover make sure you re-examine to ensure you’re not missing a long opportunity.

This premium math may become increasingly important as the Bitcoin ETF drives further BTC price action - the value of MSTR is state-dependent.

In a bitcoin bear market, it is a jerry-rigged publicly traded Bitcoin vehicle plus some governance risk that should arguably trade at a discount.

In a bitcoin bull market, it is the financial equivalent of a perpetual motion machine - reflexivity incarnate wherein higher bitcoin prices drive → a higher premium which → allows more equity and debt issuance by MSTR that in turn results in → more bitcoin on MSTR’s balance sheet, buying pressure which can drive higher bitcoin prices, which drives → a higher premium which… (ad infinitum, or ad “until bitcoin goes down”-itum). The highest premium (by my own estimation which differs from some others) ever achieved was +200%, this is the “fundamental” basis for that kind of disconnect. And it is a fundamentally sound basis, as long as bitcoin goes up. If bitcoin goes down, see 2a.

The only possible reason why 2a would not apply would be that the market is pricing Microstrategy’s ability to issue equity, debt and whatever other instruments they come up with (and, to be fair, Saylor’s talent in coming up with new ways to buy bitcoin) in a manner that results in a premium. However, it is unlikely that outweighs the fact that in a BTC bear market the demand for these instruments would be anemic and it may end up forcing Saylor to utilize capital that could ultimately result in a “margin call”. For now, however, Saylor has done an impressive job of ensuring that doesn’t happen. As it stands, BTC could essentially take a 90%+ drawdown without MSTR being “forced to sell”. Whether copycat “bitcoin treasury companies” are as shrewd or capable remains to be seen (probably not if the investment trusts of the 1920s are any indication).

I’m making this available to all subscribers, free and paid (since it was already free to begin with as I’ve been updating it publicly on twitter). However, any future trades that reference this thesis will be available to paid subscribers only, so consider upgrading your subscription if you haven’t already :).

Until December 25th, all free subscribers who upgrade to paid get 10% off their first year (applies to both monthly and annual subscriptions)

And even if you don’t want to, you can still check out my Microstrategy thesis from November 2021 and the year of updates that went along with it. I hope you decide to join as we grow a community of passionate investors willing to engage in our paid subscriber chat where we’ll have a robust debate about which of these trade ideas has the most merit!