Macro Memo: Spin Cycle

What Comes Out In The Warsh?

The Upshot

We remain medium-term bullish on the US economy and US equities. The US economy is strong but not overheating, and inflation concerns are likely to ease. Recent labor market data overstate the strength of the US economy. We believe that the US stock market rally will continue but will experience heightened volatility over the next three months as we contend with a new Fed chair, the push and pull of oil’s “Echo Shock”, and the more mature leg of the AI infrastructure buildout trade.

Momentum vs. Macro:

Rising inflation and rate hike concerns are the latest obstacle to the momentum trade

Downsides to Inflationary Risk

Most commodity disruption from the Iranian conflict has already peaked and allows the Fed to look through remaining price pressure

Core inflationary readings are stable and there are no signs of wage increases required to sustain excess demand

The labor market is not tight and recent payroll data overstate the rebound

What Will Warsh Do?

Nothing

Has the Market Topped? No.

The recent sell-off was an overdue flush of extreme leverage in extended momentum names. Fundamentals support a continued melt-up into late summer. We will see a higher incidence of 10-15% drawdowns off highs over the next 3-4 months.

Our Latest Macro Trades

Momo vs. Macro

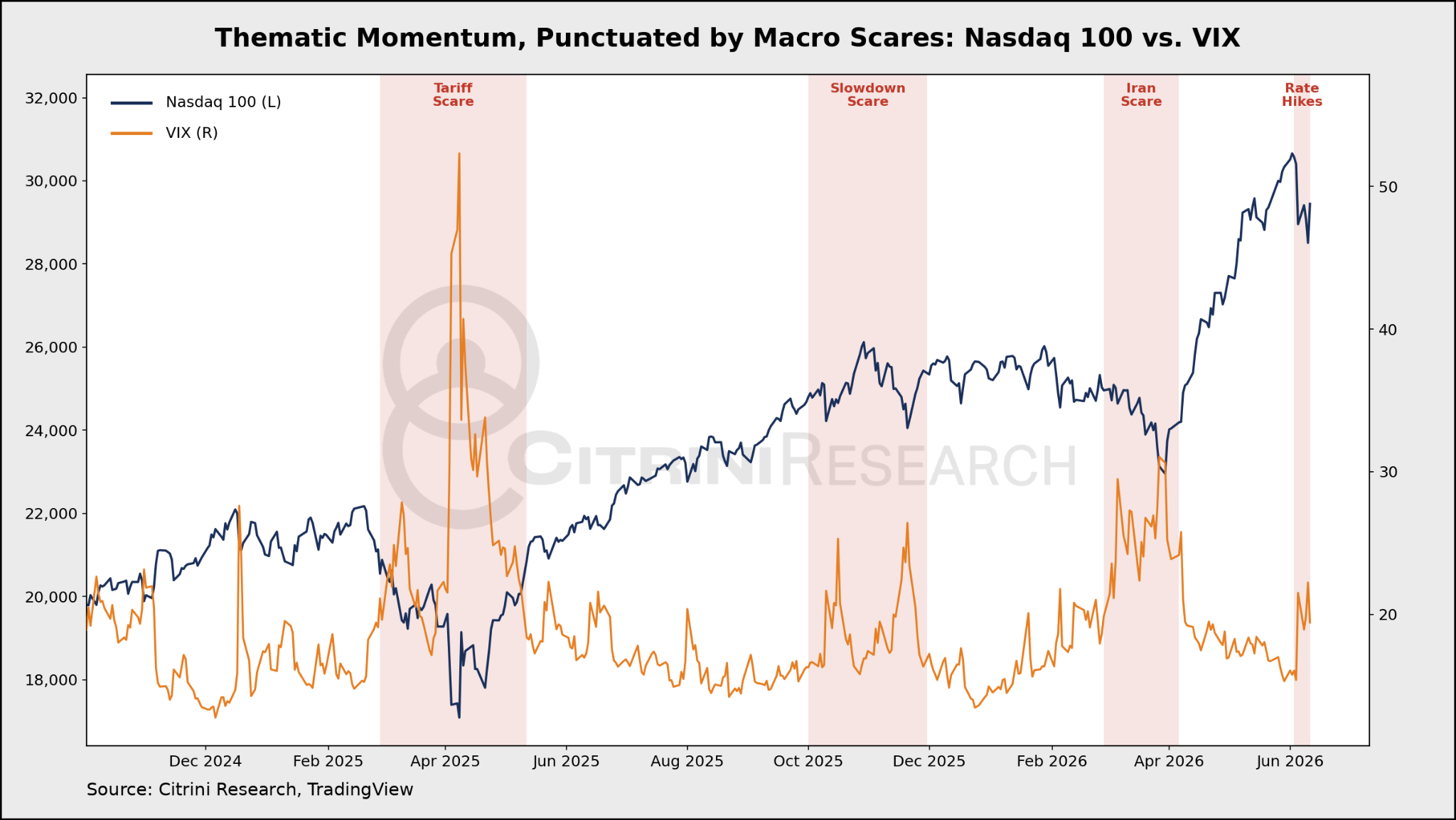

We are in a perpetual “thematic momentum vs. macro conditions” market. That is to say, we oscillate between periods of strong equity performance (largely driven by AI) and brief periods of volatility that are chalked up to macro concerns (at least on paper).

Last year was tariffs in the spring and a growth scare into the winter on the back of a series of negative payroll prints. This year, the Iran conflict put the indices on the edge of a technical correction, before an early April ceasefire sent the market ripping to all-time highs.

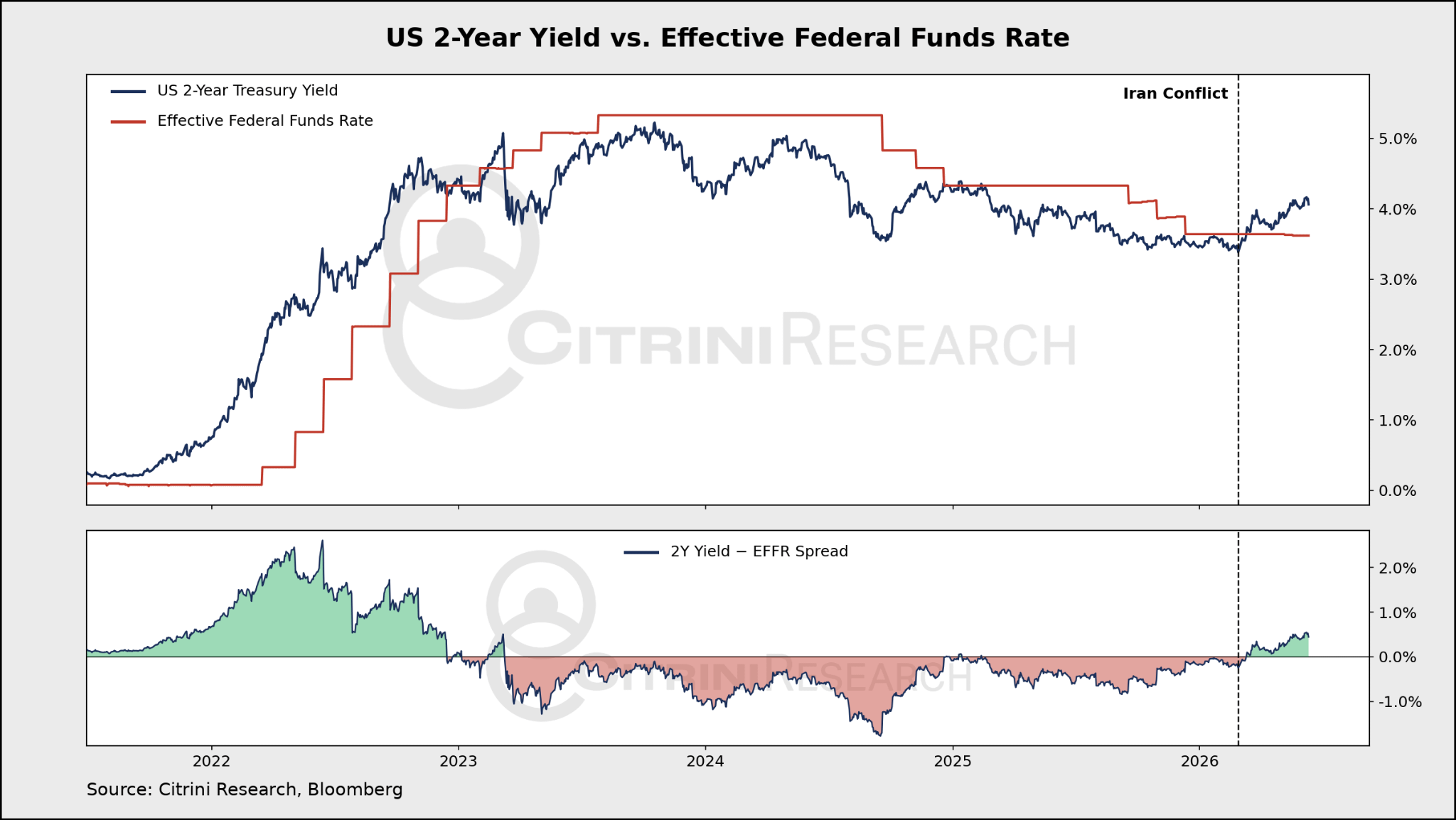

The latest macro concerns have shifted towards inflation and interest rates. Since the war with Iran began on February 28, short-term interest rate expectations have jumped by over 100bps. In May, SOFR futures began pricing in near-term rate hikes for the first time this cycle.

This is a notable monetary development and one that the market hasn’t seen since early 2023 before Silicon Valley Bank collapsed and put a final nail in the hawkish coffin.

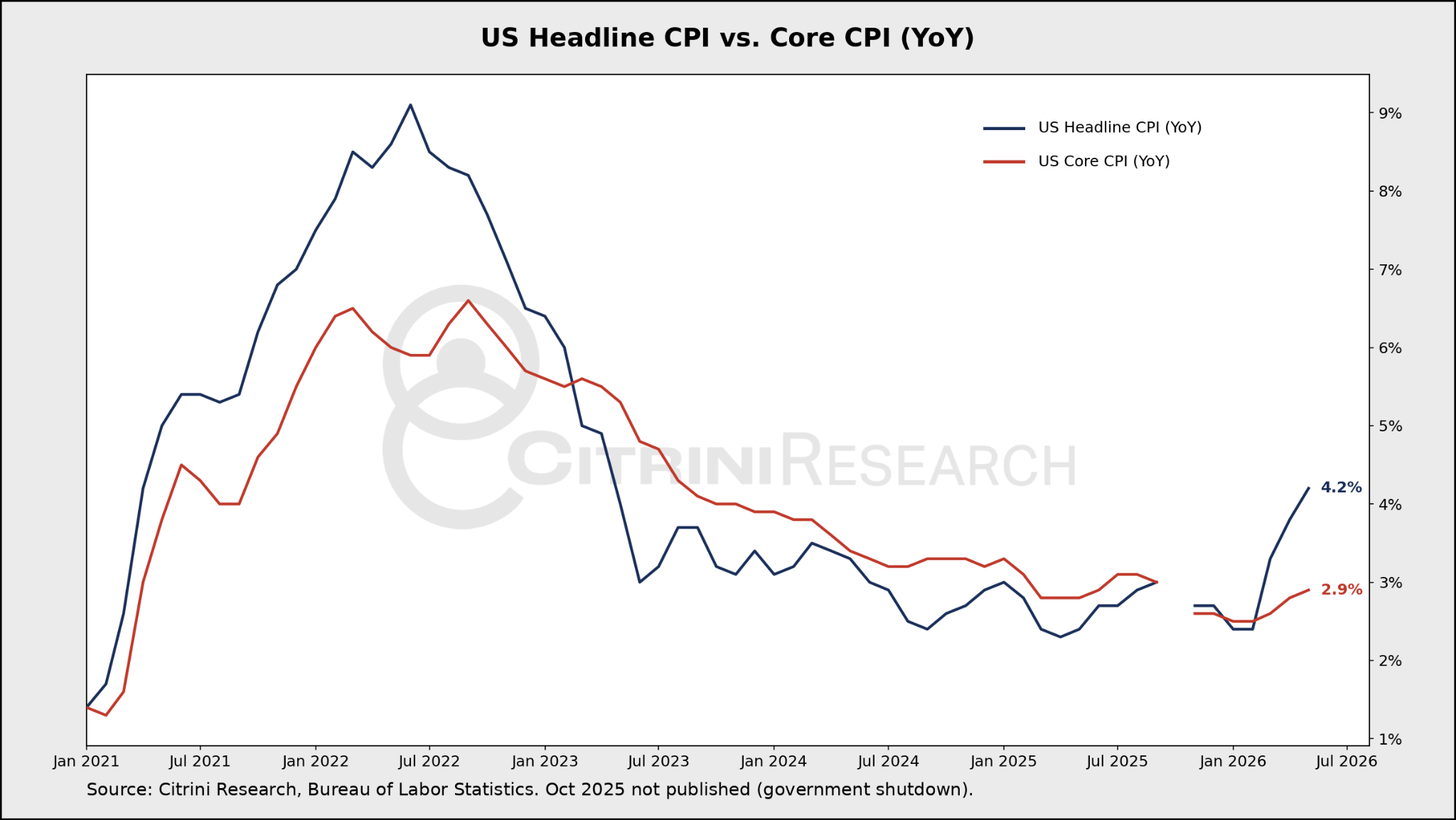

This sudden U-turn in monetary policy expectations is being driven by (1) an uptick in inflation readings exacerbated by the Hormuz-related energy shock, (2) strengthening labor market data, and (3) hawkish central bank actions in response.

The April FOMC decision to hold rates was split in a highly unusual 8-4 vote with three members wanting to remove the longstanding “easing bias” from the policy statement (Miran was the sole dissenting dove). Last week, the ECB hiked 25bps and threatened another hike as soon as July, arguing they could not “look through” the impact of rising energy costs.

This week, CPI printed the highest headline reading since 2023. All of a sudden those 1970s overlays started to look a little more concerning.

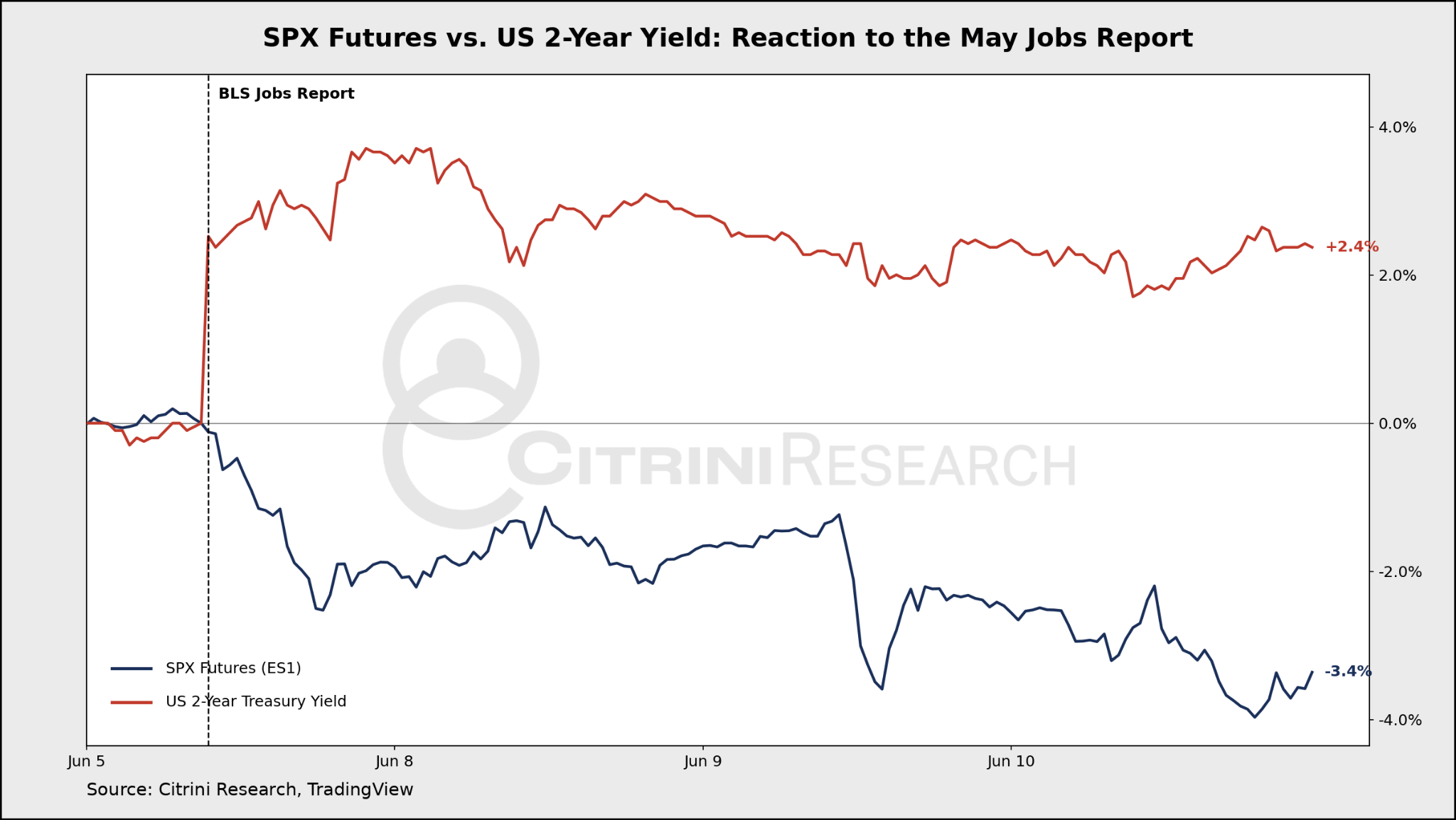

The equity market shrugged off rising rates for a while, but it seems to now be paying closer attention. The May jobs report showed 172,000 new jobs, nearly double the consensus estimate of 88,000 and much higher than the so-called “whisper number.” This adds to a string of significant employment beats and increases the market’s expectation that the Fed will hike.

US Treasury yields jumped and stocks got dumped, with the most momentum-driven names taking the brunt.

To be clear, even if rates provided an initial catalyst, a sell-off of the US stock market was unsurprising and overdue. The stock market had been on a continuous tear, rising for seven weeks straight. The sell-off was concentrated in the tech sector, specifically hardware, or momentum names. It was extremely overbought by all indicators, to the extent that it just didn’t take much of anything negative to tip it over.

We expected the drawdown to last a bit longer (and it might), but at the end of the day it is occurring in a macro backdrop that’s more sanguine than many investors think.